Most lenders run collections on disconnected tools — one for field visits, another for telecalling, a third for reporting. The coordination cost shows up in recovery leakage, manual reconciliation, and decisions made on stale data. The RBI’s Financial Stability Report projects gross NPAs rising to 3% by March 2026, signaling that pressure on collections operations is not lessening anytime soon.

A unified collections platform closes the coordination gap — giving every team, from field agents to collections heads, a single operational view with no reconciliation lag. This guide covers what to evaluate, and what to press vendors on, before you decide.

What Features to Look for in Debt Collection Software

1. Geo-Tagged Field Visit Tracking

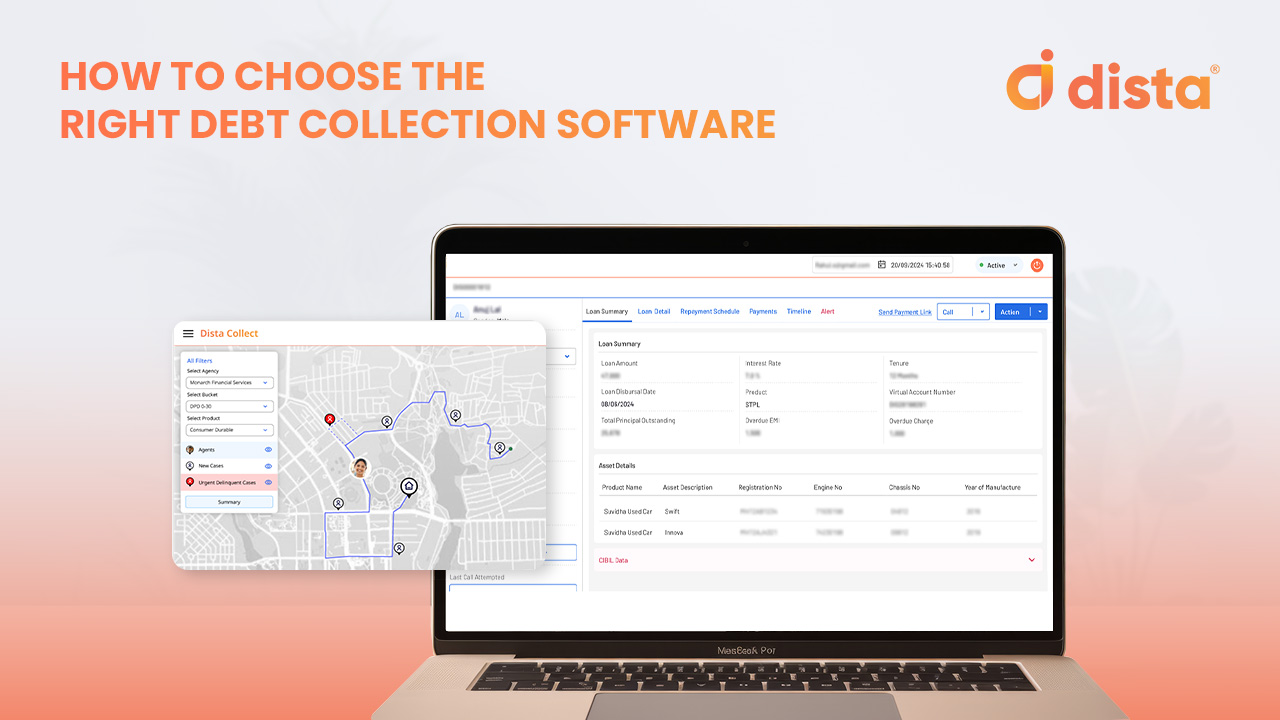

In India, as borrowers move ahead in their DPD-buckets, field collections become essential. Even home loan, vehicle finance, and microfinance collections still depend heavily on in-person visits. The platform should give field agents a mobile app that captures geo-tagged visit data without requiring manual reports.

Key capabilities to look for:

- Precise location capture with photo and borrower signature at point of visit

- Dynamic beat planning and real-time route optimization to reduce dead miles

- Offline functionality with automatic sync once connectivity returns

- Live manager visibility into field outcomes, not end-of-day summaries

2. Rule-Based Workflow Automation with AI

A platform that requires manual intervention at every case escalation will not scale. Look for configurable, rule-based workflows that adapt automatically to borrower behavior, DPD (Days Past Due) buckets, and risk segments.

What automation should handle without manual input:

- Triggering borrower communications based on DPD thresholds

- Escalating unresolved cases to the next recovery stage

- Reassigning follow-ups when an agent misses an action deadline

- Moving accounts between soft and hard bucket queues based on defined logic

3. Omnichannel Communication from One Interface

Agents switching between tabs to send an SMS, log a call, and update a case status lose time and create gaps in the interaction record. A strong platform consolidates all channels into one interface.

The communication stack should include:

- SMS, WhatsApp, email, voice, and IVR from a single dashboard

- Click-to-call with automatic outcome tagging post-call

- Auto-logging of every borrower interaction for audit readiness

- No manual case update required after a communication is sent

4. A Unified Borrower View

Repeat borrower contact is almost always a data problem. Agents end up dialling into active PTP cycles, or visiting borrowers whose accounts closed digitally days earlier, because no single system holds the complete picture. The platform should surface account status, interaction history, and field outcomes in one live view — accessible to every agent, at every touchpoint. A complete borrower profile should include:

- Account details and loan summary for baseline context

- Full payment history to identify patterns and missed commitments

- Communication logs to prevent duplicate outreach

- Field visit outcomes showing what was attempted on-ground

- PTP status to flag accounts already in a promise cycle

- Bucket segmentation to guide the right next action

5. Security and Compliance Infrastructure

Debt collection involves sensitive borrower data and direct regulatory scrutiny. Compliance should be enforced at the platform level, not managed manually by supervisors.

Minimum requirements:

- SOC 2 Type II certified and ISO 27001:2022 compliant

- End-to-end data encryption

- Role-based access controls and multi-factor authentication

- RBI Fair Practices Code enforcement built into the platform

RBI rules around contact hours, communication frequency, and borrower consent are non-negotiable. The platform should enforce them by default, with configurable parameters for your specific portfolio type.

Questions to Ask Any Vendor Before You Commit

|

Question

|

What a Strong Answer Looks Like

|

|---|---|

|

Can you show verified visit data in real time, including geo-tag and photo proof? |

Live demo with actual field data, not a screenshot |

|

How does the platform handle bucket reassignment when DPD status changes mid-cycle? |

Automated rule trigger, no manual override needed |

|

What does RBI compliance enforcement look like — configurable or hardcoded? |

Configurable by portfolio type with full audit log |

|

What is API response time for LMS integration under production load? |

Defined SLA with reference client on similar stack |

|

Can individual modules be deployed independently? |

Yes, with documented standalone deployment process |

|

What does the audit log cover, and how is it exported for regulatory review? |

Full interaction history, exportable in regulator-ready format |

Use this as a filter, not a formality. Vendors who cannot answer with specifics are worth deprioritizing.

The Cost of Running Collections on Disconnected Tools

Running separate systems for field, tele, and analytics means manual data reconciliation, version conflicts, and reporting delays. It also means your collections head is making decisions on yesterday’s data. The cost is real — in agent hours, in missed escalations, and in recovery leakage from accounts that fall through coordination gaps.

Dista Collect is a unified debt collection management platform built with location intelligence at its core. It covers field force management, omnichannel borrower engagement, automated workflows, and analytics in a single low-code/no-code environment. Banks, NBFCs, and MFIs use it to increase collection throughput, reduce manual overhead, and maintain clean compliance records.

To see how it works in a live collections environment, request a demo with the Dista team.