Given the intricacies of collections in NBFCs and MFIs, the question is not which channel, field or digital, is better. It is about building a model that deploys each channel at the right stage, based on borrower context and delinquency profile.

Dista Collect is a location-first unified debt collections CRM designed for banks, NBFCs, and microfinance institutions to manage the end-to-end debt collection lifecycle and boost recovery rates.

The platform runs on two intersecting capabilities:

- Customer 360: Identifies who the borrower is through their repayment patterns, behavioral risks, and communication preferences

- Location Intelligence: Enables field orchestration backed by insights on where, when, and how teams engage in the field

Step 1: Lead Ingestion and Data Unification

Borrower data like loan details, DPD history, promise-to-pay (PTP) records, and payment mode preferences are pulled directly from the LMS through system integration.

This eliminates manual case entry and information silos between telecalling teams and FCEs before the first contact is made.

This eliminates manual case entry and information silos between telecalling teams and FCEs before the first contact is made.

Step 2: DPD-Based Case Prioritization

The system segments borrowers by delinquency stage, repayment behavior, and risk profile.

Buckets are created based on business rules that determine whether an account gets automated outreach, enters the telecaller queue, or requires field collections activation.

Step 3: Automated Outreach for Early-Stage Accounts

When a borrower’s case enters the LOS, Dista Collect triggers:

- Context-aware communication via digital channels and Customer 360

- Location-based agency assignment, so the right agent is already mapped to the account before any escalation is needed

- Strategy Builder to configure outreach sequences by DPD bucket and repayment pattern

Step 4: Telecaller Engagement with Full Context

When the borrower confirms payment, Dista Collect acts instantly without any manual follow-up. The telecaller works from a complete view of the borrower before the call:

- A 360° customer view covering loan details, PTP history, prior interactions, and contact preferences

- Secure payment links sent instantly via the borrower’s preferred channel on confirmation

- Customer 360 updates the CRM automatically — no manual logging

Step 5: Verified Handoff to Field

Cases that could not be resolved through digital outreach and require a physical visit are escalated to field collections with complete context — last contact date, PTP status, and prior visit history.

This also helps eliminate duplicate visits on resolved cases.

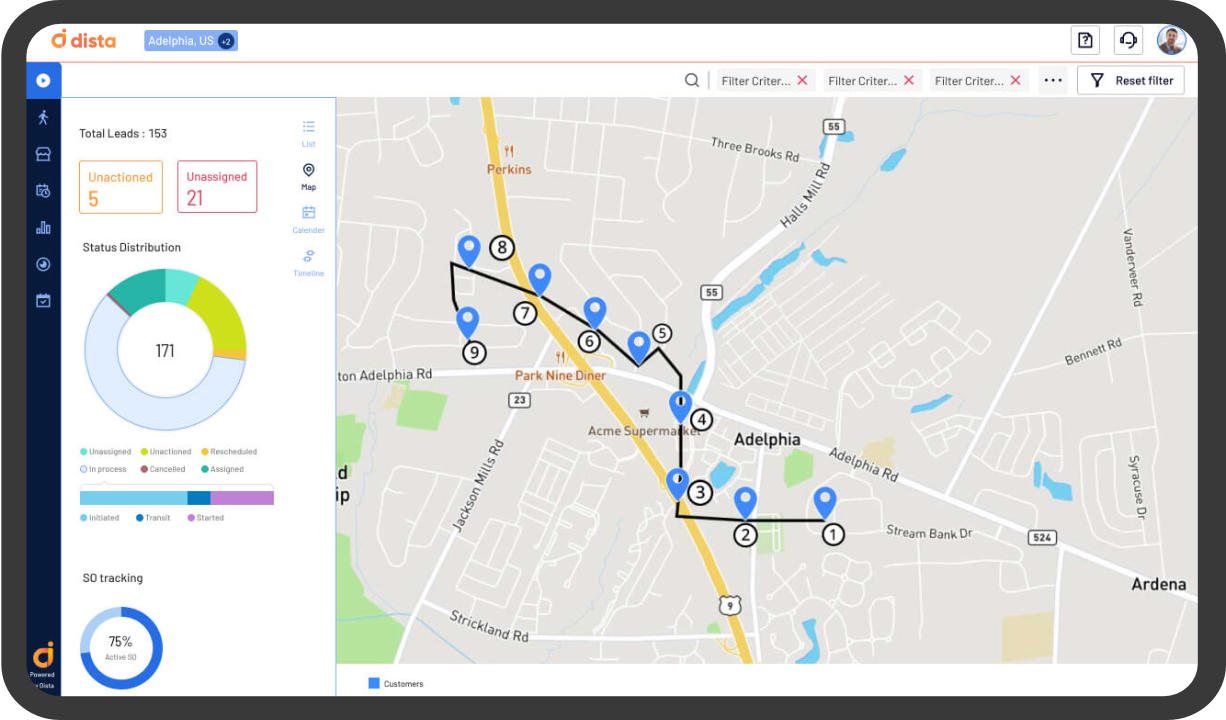

Step 6: Location-Intelligent Field Activation

When the borrower misses a second EMI, the case is allocated to an agency and FCE based on 30–60 DPD recovery logic, with an optimized beat plan and Customer 360 in hand. On the ground, this means:

- Intelligent case allocation to the right agency and FCE based on 30–60 DPD recovery logic

- Smart beat plans with optimized routes so field executives spend more time with customers

- Disposition tracking across every interaction

- Leadership insights and zone-level performance visibility for managers as it happens

- Hyper-localized clustering to identify delinquency concentration within territories

- Incentive management to drive field team performance

- An audit trail and risk compliance at every step

Read More: How Location Intelligence is Transforming NBFC Field Operations

Step 7: Settlement, Repossession, and Compliance

When the borrower does not respond to manual or digital follow-ups, the case moves into recovery. Dista Collect manages this end-to-end:

- Instant digital settlement links issued within business rules

- Digital consent management and agent-triggered repo initiation

- Asset geo-tagging, yard coordination, and auction management

Every interaction from pre-due to disposal is part of a secure, compliant trail — featuring geo-tagged visits and disposition logs, number masking, encrypted access, and RBI compliance.

Learn More: Leading NBFC-MFI Strengthens Field Collections with Location-First Intelligence