India’s microfinance sector is instrumental in ensuring financial access at the grassroot level, spanning a varied economic strata with unique needs. As of March 31, 2025, MFIs in India serve over 8 crore clients with a loan portfolio of ₹3.81 lakh crore. Every rupee of that portfolio moves through a field agent.

Yet the infrastructure built to support field agents rarely matches what the role demands on the ground. Most institutions invest heavily in credit models, risk frameworks, and compliance systems — while the operational layer that actually touches borrowers remains an afterthought.

The result: agents manage lead pipelines, run fixed center beats, handle ad-hoc recovery visits, verify post-disbursal fund utilization, and flag early stress signals across dispersed geographies — with a spreadsheet and a phone.

The gap between what the MFI field agent role demands and what institutions give agents to work with is a major reason why portfolio health suffers.

Also Read – Top 5 Location Intelligence Use Cases for NBFC and MFI

Who Is an MFI Field Agent?

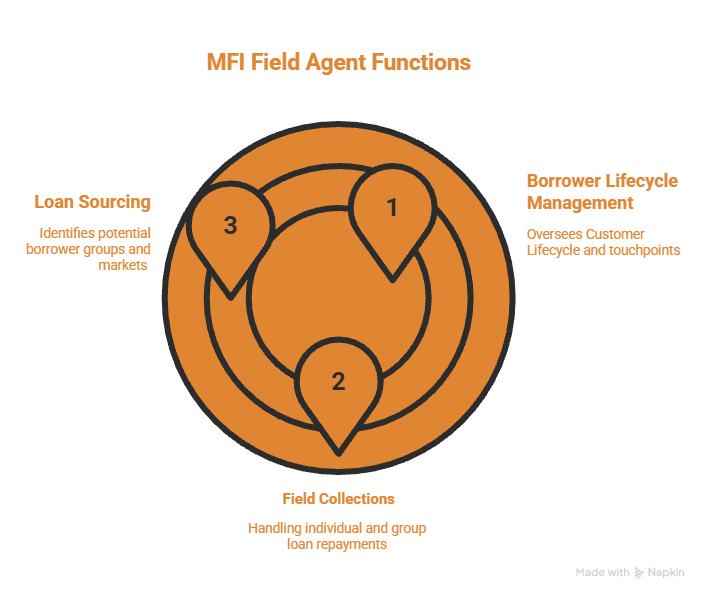

Also referred to as a loan officer, field executive, or field officer, an MFI field agent handles last-mile customer touch points across three core functions: loan sourcing, field collections, and borrower lifecycle management. Together, they make the field agent simultaneously a salesperson, a collections officer, a compliance checkpoint, and the institution’s primary data collection mechanism — all within the same working day.

Function 1: Lead Sourcing and Customer Onboarding

The problem

Microfinance lending in India is predominantly built on the Joint Liability Group (JLG) and Self Help Group (SHG) models, where groups of borrowers take collective responsibility for each other’s loans.

However, loan origination begins well before any loan is sanctioned:

- For group lending, village surveys to identify viable micro-markets, prospecting and group formation, center identification

- For individual loans, it involves serving eligible borrowers within existing groups.

At present, most of this happens without structured data. Decisions are either based on an agent’s familiarity with the area or a manager’s intuition about where to expand.

Even JLG formation may happen without an insight into existing credit density, delinquency patterns in the area, or competing MFI presence. At a small scale, this is workable, but when you amplify it across thousands of agents and hundreds of branches, the inefficiencies compound.

How Dista Manages Lead Sourcing and Borrower Onboarding

Dista brings origination workflows to the same level of rigor as collections.

- Structured lead management, OTP-verified entries, and follow-up pipelines.

- Micro-market mapping to make branch and center decisions data rather than instinct-driven.

- Territory insights to give managers a real-time view of resource utilization.

See it in Action – Top MFI Drives Loan Origination & Collections with Location Intelligence

Function 2: Field Collections and Repayment Management

Field Collections is the highest-frequency function in a field agent’s week — and the one with the most direct impact on portfolio health. The core rhythm is fixed: agents visit their assigned JLG centers — typically the same location, same time, same day each week — for group repayments.

Ad-hoc visits are layered on top. Once an individual loan is disbursed, the manager assigns recovery visits case by case, which many MFIs interlace within the agent’s existing center route.

The Operational Gap

- An agent running five center beats a day while absorbing three to four ad-hoc IL visits has no reliable way to sequence these efficiently without route optimization.

- High-DPD cases are often missed because the routing logic doesn’t account for them.

- Beyond scheduling, cash reconciliation without digital tools creates audit risk that scales directly with headcount.

- Visit compliance is a separate problem altogether. Did the agent actually meet the borrower? Is the disposition recorded accurate? Does the documentation meet RBI norms? At scale, there is no reliable way to know.

How Dista Helps with Field Collections and Repayment Management

- Route optimization sequences fixed center visits and ad-hoc IL visits into a single daily plan, reducing travel time without deprioritizing high-DPD cases.

- AI-enabled case clustering allocates recovery visits to agents based on availability, geography, and portfolio familiarity.

- Geo-fenced visit validation and photo-verified dispositions close the visit compliance gap.

- Contextual nudges sent directly to the agent’s phone prompt the right document collection at each visit, keeping RBI compliance operational.

Function 3: Customer Engagement and Lifecycle Management

A field agent’s relationship with a borrower runs deep and has multiple touchpoints.

- Initial assessment of creditworthiness

- Disbursement and post-disbursal follow-through

- Active repayment monitoring

- Renewal or graduation to an individual loan

The field agent is also the institution’s primary data collection mechanism across this entire arc.

The Operational Gap

- Post-disbursal visits are essential to verify fund utilization.

- Without structured prompts and mandatory field capture, they become check-ins with no evidentiary value.

- Agents who stay engaged across the lifecycle are best positioned to grow their portfolio — identifying renewal candidates, flagging stress early, recommending IL graduation.

- Lack of data infrastructure can often lead to missed opportunities.

- Field officer attrition in the sector runs close to 40%, according to Sa-Dhan data — when an agent leaves, everything they knew about their borrowers leaves with them.

- Without a structured mobile app, data is prone to errors, delays, and misreporting that compound across thousands of agents.

How Dista Helps with Customer Engagement and Lifecycle Management

Dista enforces data quality at source.

- Mandatory photo capture, geo-fenced check-ins, and 360° customer history accessible by loan ID and customer ID.

- Attendance, travel logs, and dispositions are unified across reimbursement workflows

- Productivity tracking reduces the administrative overhead that pulls agents away from field time.

- Dista’s web-based MIS and map-based reporting surface agent productivity, visit deviations, and portfolio anomalies — as well as the structural decisions that determine field force efficiency over the long term.

Watch – Harnessing Growth for MFIs

The Operational Case for Location-First Field Force Management

The MFI field agent carries more operational weight than the role is typically given credit for. Across a single day, the same agent sources new borrowers, runs fixed center beats, handles ad-hoc IL recovery visits, verifies post-disbursal utilization, and flags early signs of stress in their portfolio — often across dispersed geographies with minimal real-time support.

Getting this right at scale requires infrastructure that matches that complexity.

That is the operational case for a location-first approach to MFI field force management. For MFIs focused on responsible growth at the last mile, it is increasingly where technology investment is being directed.

Ready to optimize your MFI field force? Talk to the Dista team.