Key Differences and the Impact of Location Intelligence for Field Force Optimization

Non-Banking Financial Companies (NBFCs) and Microfinance Institutions (MFIs) have designed different loan systems to cater to India’s vast customer base and their specific needs. A 2023 RBI report says, NBFCs sanctioned 60% of loans digitally in 2019-20 compared to banks that sanctioned 5.6% of loans through digital channels.

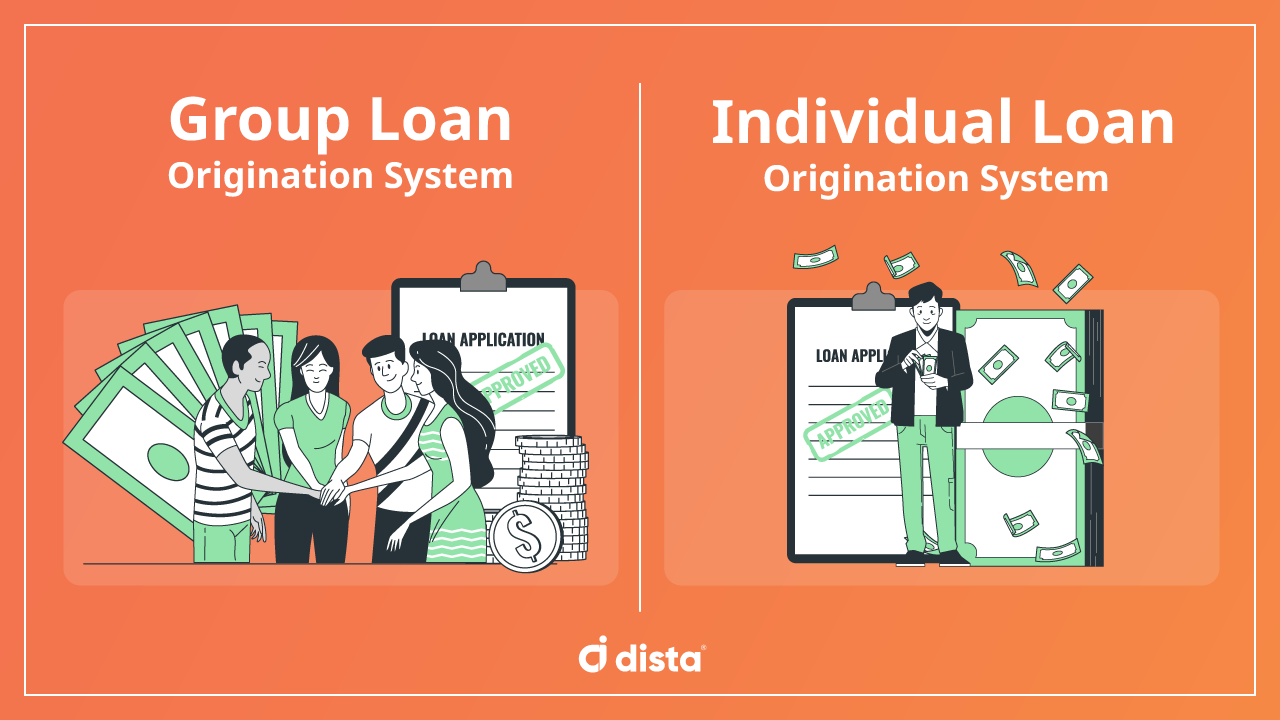

The financial institutions typically offer two main types of loans – group loans and individual loans.The Group Loan Origination System (GLOS) processes loans for a group of individuals, while the Individual Loan Origination System (ILOS) processes loans for individuals.

GLOS significantly contributes to financial inclusion in India by helping millions of people access credit. The MFI industry serves over 60 million borrowers and relies heavily on group lending models.

Both the models are critical for shaping the financial inclusivity landscape, particularly for rural and underserved communities. This blog explains the key differences between these two systems.

Group Loan Origination System (GLOS)

GLOS is widely used by MFIs in India, and is based on the principle of group lending, where a small group of borrowers apply for a loan together. The group collectively guarantees the loan repayment, reducing the risk for the lending institution.

Here are some key features:

- Group Guarantee

Instead of individual creditworthiness, the group’s collective reliability is assessed. This reduces the burden on a single borrower in case of default.

- Lower Interest Rates

Since the risk is spread across the group, lenders often offer lower interest rates compared to individual loans.

- Target Audience

GLOS is highly effective for low-income households and rural borrowers, where individual credit scores are often not available or inadequate.

- Simplified Process

Group lending usually involves simpler documentation and quicker approval, making it easier for borrowers with limited financial knowledge to access credit.

- Peer Pressure

Group lending builds a peer accountability system, where group members motivate each other to repay the loan on time.

Individual Loan Origination System (ILOS)

ILOS is designed for borrowers seeking personal loans, business loans, or other individual credit facilities. This system focuses on the borrower’s creditworthiness rather than a group.

Here are some key features:

- Personalized Assessment

Loan approvals depend on the borrower’s individual credit history, income, and repayment capability.

- Higher Interest Rates

Since the risk is borne by the individual, interest rates can be higher than group loans.

- Flexible Loan Amount

In ILOS, borrowers have more control over the loan amount based on their financial needs and repayment capacity.

- Customized Products

Lenders offer personalized products based on the borrower’s profile, which can range from personal loans to business expansion loans.

- Wider Audience

ILOS targets individuals with a stable income, good credit history, and specific borrowing needs. This system is ideal for urban borrowers and small business owners who can independently bear the loan burden.

Key Differences Between GLOS and ILOS

|

Features

|

GLOS

|

ILOS

|

|---|---|---|

|

Target Audience |

Low-income groups, rural borrowers |

Urban borrowers, small business owners

|

|

Loan Assessment |

Based on group guarantee |

Based on individual credit worthiness |

|

Interest Rates |

Lower |

Higher |

|

Loan Amount |

Fixed, smaller amounts |

Flexible, larger amounts |

|

Loan Repayment |

Group accountability |

Individual responsibility |

|

Loan Process |

Simplified |

Detailed credit assessment |

Transform Loan Origination System Process with Location-first Field Force Management

A loan origination system integrated with a location-first field force management software empowers NBFCs and MFIs by orchestrating field agent activities. The software tracks field agents activities, validates true customer visits, reduces agent travel time, and more.

In addition to orchestrating field teams, our platform strengthens key processes like loan and offerworkflows, group creation, disbursement, geo tagging, branch expansion, center creation, and more.

Take the first step towards your digital transformation journey with Dista Sales. It helps automate multiple stages of the loan origination process with location intelligence. Get in touch with us for a free demo.

In the next part of this blog, we will discuss how using location intelligence, NBFCs and MFIs can optimize and streamline loan origination processes.