Choosing the right debt collection software in India has moved from a mere IT decision to a strategic one. With retail delinquencies rising, NPA portfolios growing, and the RBI tightening operational and compliance expectations – banks, NBFCs, and MFIs can no longer afford fragmented collection stacks.

This guide compares the top 7 debt collection and loan recovery software platforms in India for 2026, these have been evaluated on the basis of AI capability, field operations, digital outreach, legal workflow automation, and RBI compliance readiness.

Quick Comparison: Top 7 Debt Collection Software in India (2026)

| Software | Best For | Key Strength | RBI Compliant |

|---|---|---|---|

|

Dista Collect |

Banks & NBFCs (end-to-end) |

AI + Location Intelligence |

Yes |

|

Credgenics |

Banks, NBFCs, ARCs, Fintechs |

Legal + digital-first recovery |

Yes |

|

FinnOne Neo Collections |

Large banks & NBFCs (legacy/on-prem needs) |

80+ API integrations, enterprise configurability |

Yes |

|

LeadSquared |

Early-stage collections |

CRM + field agent productivity |

Yes |

|

Vymo CollectIQ |

High-volume field operations |

Intelligent guided workflows |

Yes |

|

Mobicule |

Telecom, BFSI, utilities |

Modular, integration-ready |

Yes |

|

goCollect (Credility) |

NBFCs & MFIs (field-intensive) |

Smart auto-allocation + UPI receipts |

Yes |

The Top 7 Debt Collection Software Platforms in India

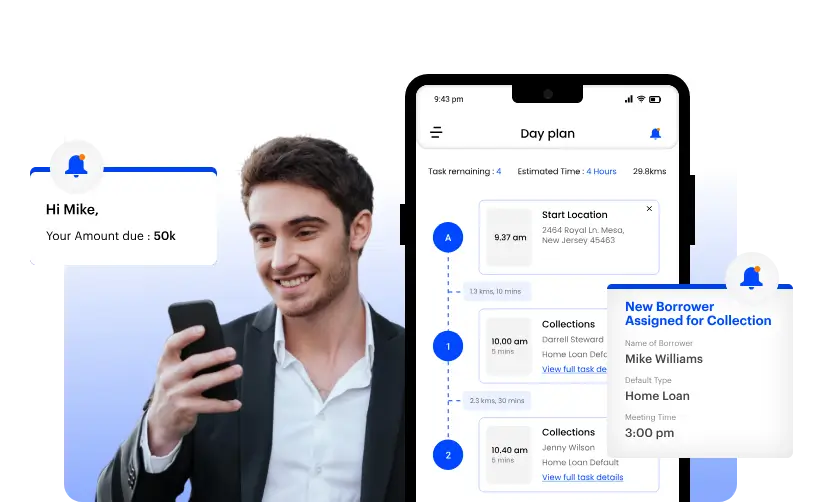

1. Dista Collect

Dista Collect is a location-powered, unified, end-to-end debt collection CRM, purpose-built for Indian banks and NBFCs. It brings together AI-driven case allocation, location-powered field force orchestration, strategy manager, digital borrower outreach, and real-time performance monitoring onto a single RBI-compliant CRM — eliminating the need for multiple point solutions across the collections stack.

Dista Collect manages the complete debt lifecycle — from pre-delinquency through settlement, repossession, and disposal — giving lenders complete visibility and control across every bucket, every team, and every channel.

Proven Results

- 85% increase in case actioning for a leading NBFC

- 35% increase in true visits through geo-intelligent agent routing

Why Choose Dista Collect?

- AI + Location Intelligence: SPACE-based allocation assigns the right case to the right field agent based on proximity, skill, and risk score

- End-to-End Lifecycle Management: Handles DPD workflows, repossession + disposal pipelines, and resource forecasting in one unified system

- Centralized Team Coordination: Unifies agency networks, telecallers, and on-ground field agents under a single command view

- Complete BFSI Visibility: Single-pane dashboard across the entire collections lifecycle from pre-delinquency to settlement and repossession, giving leadership real-time portfolio intelligence

- Audit-Ready RBI Compliance: Built-in compliant audit trails and documentation workflows that support regulatory reporting without manual effort

- Strategy Builder – Context-aware communication via digital channels and Customer 360 and Location-based assignment to the right agency even before delinquency occurs

Best For: Mid-sized to large Banks, NBFCs and NBFC-MFIs that need a comprehensive, AI-driven, location-intelligent, and audit-ready platform.

2. Credgenics

Credgenics is a SaaS-based platform supporting banks, NBFCs, MFIs, and fintechs across the debt collections lifecycle. Its competitive moat lies in legal recovery — specifically SARFAESI case management, Section 138 litigation tracking, and advocate performance monitoring — making it perfect for lenders with heavy legal escalation workflows or ARC portfolio management needs.

Why Choose Credgenics?

- Legal Workflow Automation: Tracks Section 138, Arbitration, and SARFAESI cases in real-time — including hearing reminders, notice generation, and advocate performance monitoring.

- Omnichannel Digital Outreach: Automates borrower communication across SMS, WhatsApp, IVR, voicebot, email, and self-service payment portals.

- GenAI + Predictive AI: Uses behavioral segmentation and payment-intent prediction to prioritize accounts and personalize recovery journeys.

- CG Collect Field App: Multilingual mobile app with geo-tracking, route planning, OTP-based payments, and offline support for field agents.

Best For: BFS organizations where legal escalation management and digital-first outreach are the primary operational priorities — rather than full-lifecycle field operations.

3. FinnOne Neo Collections (Nucleus Software)

FinnOne Neo Collections is a deeply configurable, workflow-driven debt recovery platform. It is used by institutions largely because of its ability to integrate deeply with complex core banking environments and legacy infrastructure that newer platforms may not support.

Easy configurability and deep integration capabilities make it most relevant for institutions where existing system compatibility is the dominant procurement constraint.

Why Choose FinnOne Neo Collections?

- Deep Integration Ecosystem: 80+ APIs for connection with core banking systems (including Finacle), LOS, LMS, and third-party services.

- Enterprise Configurability: Supports classification queues, champion-challenger strategies, rule-engine-driven scripts, and configurable allocation across agent types

- Pre-Delinquency + Delinquency Coverage: Manages early-warning outreach and full delinquency workflows in a single platform

- Legal + Repossession Modules: Dedicated workflow-driven modules for SARFAESI, Section 138 litigation, repossession, asset sale, and settlements

- mCollect Field App: Enables UPI, AEPS, debit card, and cash collections on mobile with real-time sync and geo-tracking

Best For: Institutions where deep legacy system integration and enterprise configurability are the primary constraints — and where proven institutional credibility outweighs the need for cutting-edge AI or location intelligence.

4. LeadSquared Collections CRM

LeadSquared is a debt collections CRM optimized for enhancing field agent productivity and early-stage recovery. It combines borrower segmentation, automated recovery workflows, real-time field tracking, and day-planning tools that help agents optimize daily routes while giving managers live visibility into performance.

Why Choose LeadSquared?

- Real-Time Field Visibility: Live agent tracking and performance dashboards with granular productivity metrics

- Mobile-First Task Management: Structured daily workflows optimized for on-ground collection agents

- Automated Communication Flows: Triggers reminders, alerts, and follow-ups across email, SMS, and call channels based on borrower behavior

Best For: Lenders focused on Bucket 0–1 early-stage collections with structured, CRM-driven agent workflows and mobile-first operations.

5. Vymo CollectIQ

Vymo CollectIQ is an end-to-end collections platform designed for lenders running tightly coordinated, high-volume field recovery operations. It combines intelligent nudges, guided workflows, and integrated incentive management to keep large field agent networks accountable and productive.

Why Choose Vymo CollectIQ?

- Mobile-First Field Platform: Designed specifically for agents operating on the ground across high-volume portfolios

- Intelligent Nudges & Guided Workflows: Surfaces the next-best action at every stage of a field visit — reducing agent decision fatigue

- Incentive & Performance Management: Builds field accountability through transparent, data-driven incentive tracking

Best For: Organizations managing high-volume, field-intensive recovery operations across large, geographically distributed agent networks.

6. Mobicule

Mobicule offers a modular debt collection platform designed to digitize recovery operations across telecom, BFSI, and utilities sectors. It supports case allocation, digital payments, repository workflows, and detailed audit trails — making it particularly strong for organizations with complex, industry-specific compliance requirements.

Why choose Mobicule?

- Industry-Specific Compliance: Purpose-built audit features addressing the unique regulatory environments of telecom, utilities, and BFSI

- Modular Architecture: Choose only the modules needed — scale the platform as operations grow

- Integration-Ready: Connects seamlessly with existing LOS, LMS, and core banking infrastructure

Best For: Enterprises in telecom, utilities, and BFSI that need a modular, compliance-ready, and integration-friendly collections platform.

7. goCollect (Credility)

goCollect by Credility is a smart, automated debt collection platform built specifically for field-intensive NBFCs and MFIs. Its intelligent case auto-allocation engine assigns the right agent to the right borrower based on profile analysis — ensuring high-priority accounts are never missed and every PTP (Promise-to-Pay) follow-up is tracked.

Why Choose goCollect?

- Smart Auto-Allocation: Analyzes borrower profiles and automatically assigns cases to the most suitable field agent — eliminating manual allocation delays

- Multi-Channel Digital Outreach: Integrates WhatsApp, SMS, robocalls, and email via a dynamic communication engine

- Real-Time Receipting: Automatically generates and sends payment receipts via SMS or email the moment a collection is made — with support for UPI, cash, cheque, and DD

- Granular Performance Tracking: Tracks agent productivity at individual, branch, cluster, region, and pan-India levels in one view

Best For: NBFCs and MFIs running field-intensive collections where agent accountability, smart allocation, and real-time reconciliation are the primary operational needs.

Why Indian BFSI Enterprises Are Replacing Legacy Systems in 2026

The RBI Financial Stability Report consistently flags rising retail delinquencies and accelerating digital adoption as structural pressure points for India’s lending ecosystem. For collection heads, this translates to four recurring operational failures:

- No single source of truth across field agents, telecallers, agencies, and legal teams

- Operational inefficiencies driven by siloed CRMs, standalone tracking apps, and disconnected telecalling tools

- Delayed action on delinquent accounts due to poor risk-based case prioritization

- Compliance gaps in borrower communication audit trails, DND controls, and SARFAESI documentation

These aren’t technology gaps — they’re structural ones caused by running 3–5 disconnected systems that don’t talk to each other.

Unified debt recovery software solves this by consolidating the entire collections lifecycle — from Bucket 0 digital outreach to NPA legal escalation, field operations, agency coordination, repossession, and compliance tracking — into a single, intelligent platform.

How to Choose the Right Debt Collection Software for Your Organization

Selecting a debt recovery platform is not a feature checklist exercise. Here is a decision-ready framework built around your specific lending profile.

Step 1: Segment by Lender Type First

Different institution types have fundamentally different collection challenges:

- Large Banks & Enterprise NBFCs: Need AI-driven prioritization, end-to-end lifecycle management, geo-based field operations, and complete portfolio visibility. Dista Collect is the strongest fit, with FinnOne Neo as an alternative for institutions where deep legacy system integration is the binding constraint

- Mid-Sized NBFCs: Need intelligent case allocation, DPD workflow automation, and real-time field coordination. Dista Collect and Credgenics are the leading options

- MFIs & Smaller NBFCs: Need mobile-first, lightweight platforms with smart allocation and real-time receipt. For larger MFI networks with more complex portfolio structures, Dista Collect is worth evaluating

Step 2: Match Software to Your Collections Stage

- Bucket 0–1 (Early Stage): Prioritize automated digital outreach, DND-compliant communications, and mobile-first agent workflows

- Bucket 2–3 (Mid Stage): Look for AI-driven case prioritization, geo-routing, field force optimization, and PTP tracking

- NPA / Legal / Written-Off: Require SARFAESI case management, Section 138 litigation tracking, hearing dashboards, and audit-ready documentation

Step 3: Evaluate Execution Intelligence, Not Just Dashboards

The best platforms go beyond reporting. Look for systems that intelligently prioritize cases based on risk score, DPD bucket, geography, and agent skill — not just ones that surface data after the fact.

Step 4: Verify Integration & Compliance Readiness

Your collection software must integrate with your LOS and LMS for real-time data sync. For Indian lenders, RBI-compliant audit trails, NACH mandate management, and DND-adherent communication controls are non-negotiable — not nice-to-haves.

Step 5: Run a Pilot on a Representative Portfolio

Before full deployment, test on a meaningful segment. Track:

- Change in case closures week-on-week

- Increase in true visits per agent

- Reduction in time-to-contact for fresh delinquencies

- Compliance audit pass rates

Step 6: Calculate Total Cost of Ownership (TCO)

Look beyond licensing fees. Factor in integration costs, implementation timelines, training, support SLAs, and the hidden cost of not automating — in missed recoveries, compliance penalties, and agent attrition.

Frequently Asked Questions: Debt Collection Software in India

Q: What is Debt Collection Software?

Debt collection software is a digital platform that helps banks, NBFCs, MFIs, and ARCs manage the end-to-end loan recovery process — including borrower communication, field agent management, case prioritization, legal workflows, and RBI compliance tracking.

Q: Which is the best Debt Collection Software in India in 2026?

For banks and NBFCs seeking a comprehensive, AI-driven, and location-intelligent platform that covers the full collections lifecycle, Dista Collect is the strongest fit. Credgenics is the specialist choice for legal escalation and ARC operations. FinnOne Neo suits institutions where legacy system integration is the primary constraint. The right choice ultimately depends on your lender type, collections stage, and portfolio complexity.

Q: What India-specific compliance features should Debt Collection Software support?

India-specific compliance features include: SARFAESI case management, Section 138 (NI Act) litigation tracking, NACH mandate management, RBI-compliant DND and communication frequency controls, data masking per privacy laws, audit trails for all borrower interactions, and real-time OTP-based payment verification.

Q: How does AI improve debt collection in India?

AI improves debt collection by intelligently segmenting borrower risk, predicting repayment likelihood, auto-prioritizing cases for field agents, optimizing geo-based collection routes, and triggering personalized multilingual communications — all of which increase recovery rates while reducing the cost-to-collect.

Q: What is the difference between a debt collection CRM and a full-lifecycle collections platform?

A debt collection CRM (like LeadSquared) focuses primarily on agent workflow management, task structuring, and early-stage borrower engagement. A full-lifecycle collections platform (like Dista Collect) manages the entire recovery journey — from Bucket 0 digital outreach through field operations, agency coordination, repossession, legal escalation, and NPA management — in a single integrated system.

Which Debt Collection Software is Right For You?

The debt collection software landscape in India has matured significantly — and the gap between platforms built specifically for Indian lending operations and generic global tools has never been wider.

For banks and NBFCs — mid-sized to large — seeking a truly unified, AI-driven, location-intelligent platform that covers the full collections lifecycle, Dista Collect is the most comprehensive solution available today. Its combination of SPACE-based AI allocation, geo-powered field operations, end-to-end DPD lifecycle management, and a single-pane visibility layer addresses the structural fragmentation that most Indian lenders still struggle with.

The right choice depends on your lender type, collections stage, portfolio complexity, and where your biggest operational gaps currently sit.

Ready to see Dista Collect in action?

Book a demo to see how AI + Location Intelligence transforms field collections, true visit rates, and recovery outcomes for Indian lenders.

Note – All images have been sourced from the official webpages of the concerned companies.